I have enough data to write the article now.

- The FOMC held the fed rate decision at 3.50–3.75% for a fourth consecutive meeting on June 17, 2026.

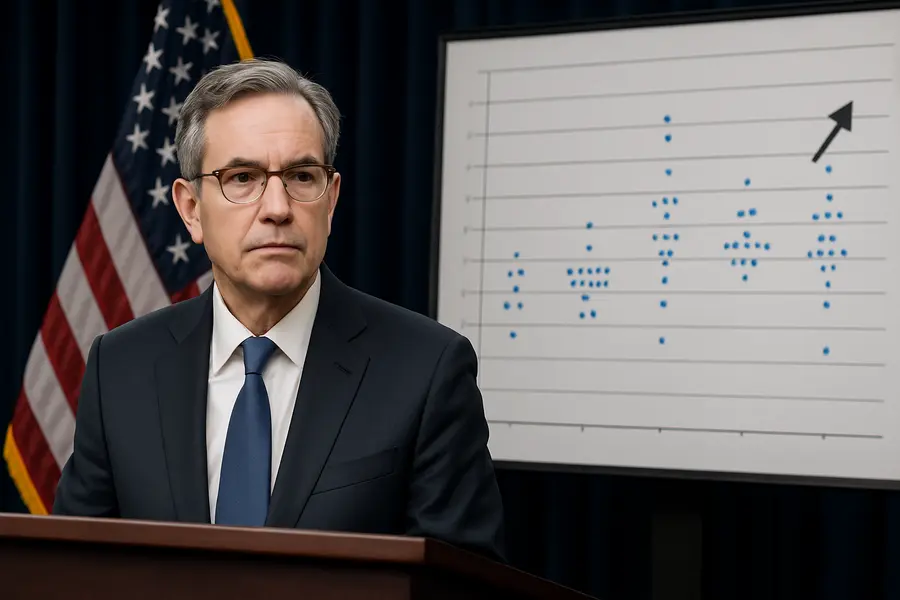

- The dot plot shifted sharply: nine of 18 officials project at least one 25-basis-point hike before year-end; the median 2026 rate forecast rose to 3.8% from 3.4% in March.

- Warsh declined to submit his own dot projection and announced task forces to overhaul Fed communications, balance-sheet strategy, and inflation frameworks.

---

The Federal Reserve held its benchmark rate steady at 3.50–3.75% on June 17 but delivered a jarring policy signal — nine officials now favor a 2026 rate hike — as incoming Chair Kevin Warsh reshaped the institution's communications from his first press conference.

Lead

The Federal Open Market Committee voted unanimously on June 17, 2026, to leave the federal funds rate target unchanged at 3.50–3.75%, extending its pause to four meetings. The rate hold itself was fully priced by markets. What was not: a dramatically more hawkish dot plot and a debut press conference from new Chair Kevin Warsh that scrapped forward guidance and signaled structural changes to how the central bank operates. The S&P 500 fell 1.21% on the day — its worst performance on any first-meeting day for a new Fed chair — while the 2-year Treasury yield surged more than 16 basis points to 4.216%.

What Happened

The June Summary of Economic Projections contained the session's real shock. The median 2026 fed funds rate forecast jumped to 3.8% from 3.4% in March, a quarter-point above the current target ceiling. Nine of 18 officials — one short of a majority — now project at least one 25-basis-point rate hike this year; six of those pencil in two hikes. Three months ago, the modal view was a single quarter-point cut in 2026. The reversal reflects a significant repricing of the inflation outlook: median PCE inflation for 2026 was revised to 3.6%, up from 2.7% in March, while core PCE moved to 3.3% from 2.7%. The median unemployment forecast was nudged down marginally to 4.3% from 4.4%.

Warsh, who was confirmed as the 17th Fed chair after being nominated by President Donald Trump, participated in his first FOMC meeting as presiding officer. Notably, he did not submit a dot-plot projection himself — only 18 of 19 officials entered forecasts — declining to anchor market expectations to a personal rate view at the outset of his tenure.

Market Reaction

Equity markets sold off sharply as investors recalibrated rate-cut expectations. The S&P 500 closed at 7,420.10, down 1.21%. The Dow Jones Industrial Average shed 507 points, or 0.98%, and the Nasdaq Composite dropped 1.34% to 26,021.66. The selloff was concentrated in rate-sensitive sectors: real estate, utilities, and long-duration growth names bore the brunt.

In fixed income, the 2-year Treasury yield — the most responsive to near-term Fed policy shifts — climbed to 4.216%, its highest close since early spring. The 10-year yield rose 7 basis points to 4.487%, steepening the curve modestly as longer-term growth expectations held more steady than short-end rate bets.

Warsh's Policy Signal

In his press conference, Warsh repeatedly invoked "price stability" as the Fed's paramount obligation, a phrasing choice that markets read as a signal he will not ease prematurely to accommodate political pressure for lower rates. He announced that the Fed had "dropped forward guidance" — the practice of telegraphing future rate moves in policy statements — a significant departure from the communication architecture established under his predecessors.

In its place, Warsh said the FOMC would adopt a purely data-dependent posture, with no explicit bias toward either easing or tightening. The June policy statement removed prior references to "additional rate adjustments," replacing them with language that commits to monitoring incoming data without signaling a directional tilt.

Warsh also disclosed the creation of several task forces to conduct wholesale reviews of Fed operations across three domains: communications strategy, the central bank's balance sheet, and its inflation-targeting framework. The reviews carry no immediate policy implications but indicate that Warsh intends to put his mark on institutional structure, not merely interest-rate settings.

Strategic Context

The hawkish dot-plot revision is grounded in a deteriorating inflation picture. Tariff pass-through and persistent services inflation have kept core PCE above 3%, well above the Fed's 2% target, despite four meetings without a rate change. The March projections had assumed a gradual drift lower; the June revisions acknowledge that disinflation has stalled.

Warsh's refusal to submit a dot projection is consistent with his stated skepticism of the format — he has previously argued that numerical rate forecasts can become self-fulfilling and reduce the committee's strategic flexibility. By withholding his own marker while encouraging others to participate, he preserves optionality without dismantling the publication entirely.

The decision to drop forward guidance aligns with a broader philosophical shift. Warsh has argued that explicit rate guidance constrained the Fed in fast-moving environments, citing the delayed response to the 2021–2022 inflation surge as a cautionary case.

What Comes Next

Markets have now largely unwound bets on a 2026 rate cut, pricing in a modest probability of a 25-basis-point hike at either the September or November meeting. The July FOMC meeting carries no projections update and no scheduled presser, keeping the September session as the next major policy inflection point.

Warsh's task forces are expected to deliver preliminary findings before year-end. A revision to the inflation framework — potentially including a rethink of flexible average inflation targeting — would be the most consequential structural change since the Fed's 2020 strategy review.

Outlook

The June FOMC meeting confirmed what Warsh's nomination implied: the era of rate-cut expectations has ended. With nine officials signaling a potential hike, PCE inflation revised sharply higher, and the new chair dismantling forward guidance, the policy trajectory has shifted from "how soon do cuts arrive" to "how high might rates go." The next catalyst is September's projections update, where a revised dot plot and Warsh's own potential debut forecast will determine whether the hawkish pivot hardens into a tightening cycle.

Mentioned tickers: SPY, QQQ, DIA, TLT, IEF, SHY