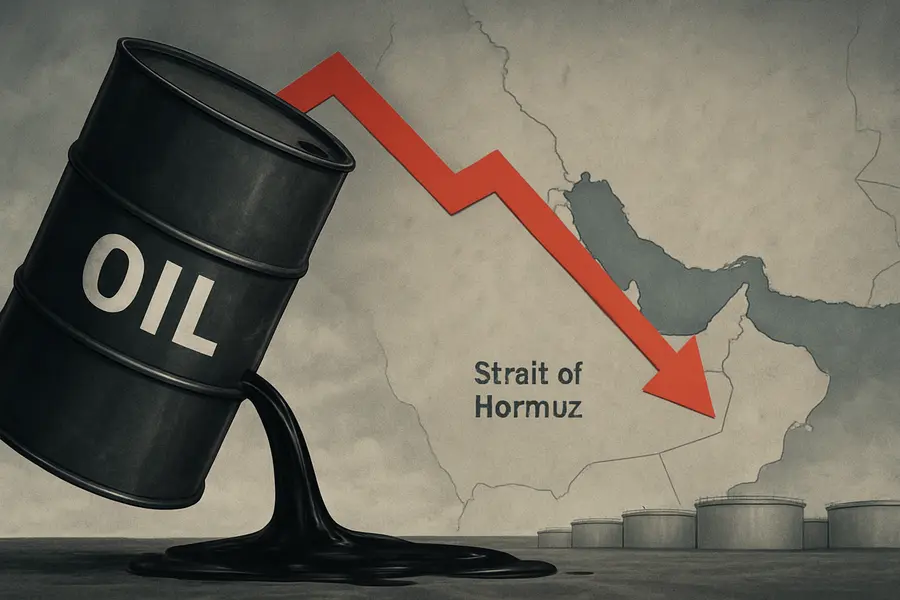

Iran's Hormuz closure removed 13.6 mb/d from global supply, sent Brent crude above $125, and pushed OECD inventories toward 20-year lows as peace talks stall in early July 2026.

- The Strait of Hormuz crisis cut 13.6 mb/d from global supply by May 2026 — the IEA's largest-ever recorded disruption.

- Brent crude surged from a January baseline near $68 to above $125 before retreating to ~$70.57 as Hormuz flows partially recovered.

- Saudi Arabia posted a $33.5bn Q1 2026 budget deficit; OECD inventories are forecast to reach their lowest level since 2003 by December.

Lead

Four months after U.S. and Israeli forces struck Iranian military infrastructure on February 28, the oil supply war set in motion by Tehran's retaliatory closure of the Strait of Hormuz has delivered the most severe energy shock since the 1970s. The crisis has reshaped global commodity markets, strained sovereign budgets, and confronted central banks with an inflation surge that monetary tightening alone cannot resolve. By early July 2026, Brent crude traded at $70.57 a barrel — more than 50% above its January baseline — as fragile diplomatic channels attempt to prevent a re-escalation and marketplace stories of recovery compete with warnings of structural damage still unfolding beneath the surface.

The Scale of the Shock

The IEA designated the 2026 Strait of Hormuz crisis as "the largest supply disruption in the history of the global oil market." The strait, through which approximately 20 million barrels per day (mb/d) of crude oil and refined products transited in 2024 — roughly one-fifth of global petroleum consumption and more than one-quarter of seaborne oil trade — was effectively choked by Iran's deployment of drones, ballistic missiles, and attack boats against transiting vessels following the initial U.S.-Israeli strikes.

Global oil supply fell 1.8 mb/d in April to 95.1 mb/d, then a further 600,000 barrels per day (kb/d) in May, bringing cumulative losses to 13.6 mb/d versus pre-conflict levels. The shock's magnitude exceeded the 1973 Arab oil embargo, the 1979 Iranian Revolution, and the combined disruptions of the 1980–1988 Iran-Iraq War.

Price Arc: Surge, Peak, Retreat

The initial strikes drove Brent crude 10–13% higher within 48 hours, to approximately $80–82 a barrel. As the Hormuz closure widened, prices accelerated toward a four-year high above $125 per barrel in late April, with analysts warning of imminent jet fuel shortages and government officials modeling scenarios approaching $200 a barrel in the event of a prolonged shutdown.

The reversal began in late June as the United Arab Emirates restored crude exports to more than 3.9 mb/d, pushing total daily Hormuz flows past 10 mb/d. Emergency strategic petroleum reserve (SPR) releases by the United States and allied nations, combined with Saudi Arabia's ad hoc discounted sales to Asian buyers, generated a near-term surplus. Brent fell below $71 on July 2 and settled at $70.57 — down 0.83% on the session. WTI crude settled near $68.50, recovering from a 2% intraday loss ahead of the U.S. Independence Day holiday weekend.

Demand Destruction and Economic Fallout

The economic news embedded in consumption data is stark. World oil demand is forecast to contract 420 kb/d year-on-year in 2026 to approximately 104 mb/d — 1.3 mb/d below pre-war projections. The petrochemical and aviation sectors absorbed the sharpest initial losses, but higher energy costs have since propagated broadly into surface transportation and manufacturing, sustaining inflationary pressure across supply chains.

Institutional oil analysis has drawn explicit parallels to the 1970s stagflation cycle. The combination of acute supply shortages, currency volatility, and rising inflation expectations weighs most heavily on oil-import-dependent economies. Asia confronts the most immediate disruption given its structural dependence on Gulf crude. Europe faces medium-term exposure, with the United Kingdom identified in multiple analyses as the most vulnerable major developed economy. OECD total liquid fuel inventories are forecast to fall to just under 2.3 billion barrels by December 2026 — their lowest level since 2003 and approximately 500 million barrels below the prior five-year average.

OPEC+ and the Saudi Dilemma

OPEC+ has navigated the crisis with adjustments that have been largely nominal. In May 2026, seven member nations agreed to a 188 kb/d production increase for June — a figure set against a backdrop in which Saudi Arabia's OPEC quota stood at 10.291 mb/d while actual output reached only 7.76 mb/d in March, reflecting physical constraints and disrupted logistics.Saudi Arabia's fiscal position captures the full complexity of the current oil analysis. Riyadh posted a $33.5 billion budget deficit in the first quarter — a record shortfall driven by war-related expenditures and revenue losses during peak price volatility. The IMF and independent economists estimate Saudi Arabia's fiscal breakeven at $80–85 per barrel; Bloomberg Economics places it as high as $96. With Brent trading in the low $70s, Riyadh faces a structurally difficult revenue environment that threatens funding for Vision 2030 infrastructure programs. In response, the kingdom has cut its official selling prices to Asian buyers to five-year lows, prioritizing volume over margin to defend market share as supply normalizes.

Diplomatic Overhang

The partial Hormuz reopening has not resolved the underlying conflict. Peace talks in Qatar, which had approached near-finalization in late June, were delayed by the state funeral of former Iranian Supreme Leader Ali Khamenei, which began July 4. Tehran has demanded permanent maritime control over the strait as a non-negotiable condition for a broader settlement — a position Washington and Riyadh both reject. U.S. President Donald Trump reiterated opposition to Iranian nuclear weapons acquisition at the holiday weekend, maintaining elevated diplomatic pressure.

Outlook

The immediate oil supply war shock is easing, but structural fragility persists. OECD inventories are severely depleted, Hormuz transit flows remain below pre-conflict norms, and the diplomatic pathway to a durable ceasefire remains contested. Current institutional forecasts place Brent's trading range for the remainder of 2026 between approximately $52 and $77 — a band that would collapse immediately on any re-escalation that shuts Hormuz again. For global economies still absorbing the fiscal and inflationary aftermath of the most severe supply disruption in market history, the buffer against a second shock is narrow.

Mentioned tickers: BNO, USO, XOM, CVX, BP, SHEL, TTE, COP, OXY, SLB