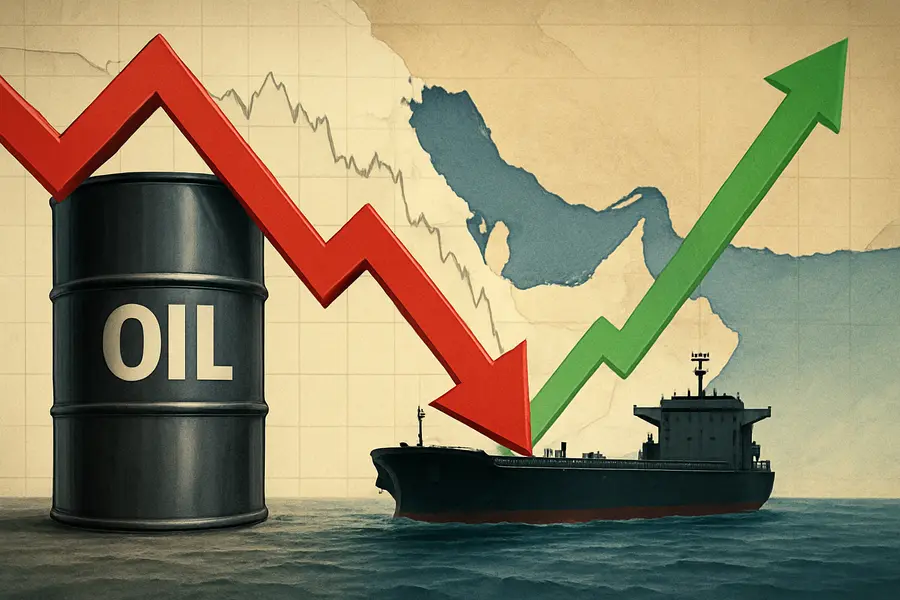

Brent crude drops to $70.57 as tanker traffic through the Strait of Hormuz tops 10 million barrels per day following the June 17 US-Iran ceasefire, erasing the entire conflict premium.

- Brent settled at $70.57/bbl on July 2 — the lowest close since before the February 28 US-Israeli strikes on Iran.

- Hormuz oil flows have recovered to more than 10 million barrels per day; traffic was near zero through April.

- OPEC+ approved its fourth consecutive output hike, adding 188,000 bpd in July for a cumulative 600,000 bpd increase since April.

Lead

Crude oil prices fell for a third straight session heading into the U.S. Independence Day holiday weekend, with Brent crude settling at $70.57 per barrel and West Texas Intermediate at $68.50 on July 2 — the deepest close since before the February 28 US-Israeli military strikes on Iran that triggered four months of disruption in global oil supply. The catalyst is a rapid normalization of tanker flows through the Strait of Hormuz, which by late June had returned to more than 10 million barrels per day after near-total paralysis earlier in the spring.

What Happened

On June 17, Washington and Tehran signed a memorandum of understanding to end the conflict and reopen the strait under a 60-day toll-free transit framework while permanent peace negotiations proceed. The agreement gave immediate relief to a global tanker fleet that had been idled in the Persian Gulf: vessels carrying roughly 35 million barrels exited Hormuz in the days immediately following the accord, and Iran has since exported more than 40 million barrels of crude — currently at prices roughly 20 percent above pre-war levels, reflecting pent-up buyer demand and constrained tanker availability.

The UAE, whose export terminal infrastructure was disrupted during the conflict, has restored throughput to approximately 3.9 million barrels per day. Combined with Iranian reflows, that has pushed aggregate daily Hormuz transit volumes past the 10-million-barrel threshold — well short of the pre-war norm of roughly 21 million barrels per day carried by as many as 138 vessels, but a dramatic reversal from the approximately 5 percent of pre-war average recorded across April.

Market Reaction

The restoration of Middle East oil supply has methodically unwound the geopolitical risk premium that pushed crude sharply higher during the conflict. Brent has fallen more than $4 since the June 17 signing and is now trading at levels consistent with the late-2025 price range. WTI touched an intraday low near $67 per barrel during Thursday's session before a modest recovery ahead of the long weekend. The moves reflect a market repricing away from scarcity and toward a supply-surplus framework.

Broader commodity markets registered the shift. Energy equities extended multi-week underperformance relative to the broader market as investors trimmed upstream producer exposure, while refining margins in Asia came under renewed pressure as feedstock availability improved.

OPEC+ and Supply Dynamics

OPEC+ has added a compounding bearish element by approving four consecutive monthly output increases totaling nearly 600,000 barrels per day since April — a deliberate strategy to capture market share during a window when Hormuz disruptions provided political cover for expansion. The July tranche of approximately 188,000 bpd takes effect as Iranian barrels simultaneously reenter the market.Saudi Arabia has also conducted ad hoc spot sales to Asian buyers at competitive differentials, in a pattern that has historically preceded broader price management efforts within the cartel. The combination of coordinated OPEC+ increases and Iranian re-export volumes is creating what analysts describe as the first genuine oil supply surplus since early 2025.

Geopolitical Dimension

The 60-day toll-free window expires in mid-August, at which point Iran will enter talks with Oman and the Gulf Cooperation Council states on future strait governance. Tehran has left open the possibility of imposing transit fees once negotiations conclude — a mechanism that would give Iran a revenue stream from the strait short of outright closure. That uncertainty is keeping some risk premium embedded in forward curves even as spot prices fall.

The interim peace deal is explicitly not a finalized agreement. Verification of Iranian nuclear commitments, the timeline for US naval force repositioning, and the legal status of sanctions relief remain under negotiation. Any breakdown in the 60-day window would reintroduce the full risk premium the market is currently pricing out.

Crude Forecast

The forward picture for crude is heavily weighted to the downside on supply fundamentals. The global market is tracking toward a surplus of approximately 3.7 million barrels per day in the second half of 2026 as non-OPEC+ output growth — led by the United States, Guyana, and Brazil — combines with Middle East normalization. J.P. Morgan's crude forecast projects Brent averaging near $60 per barrel for the full year. Scenario analysis from several investment banks places WTI at $55 per barrel or below in Q4 if Iranian volumes fully normalize and OPEC+ discipline frays.

The EIA's short-term energy outlook, last updated in June, projects a continued inventory build through year-end absent new supply disruptions, consistent with the bearish consensus range.

Outlook

Oil price today dynamics reflect a market shifting from crisis management to fundamental repricing. Brent at $70.57 and WTI at $68.50 mark the bottom of the conflict premium band; the next directional move depends on whether the US-Iran interim deal survives its 60-day negotiating window and whether OPEC+ has the cohesion to cap the output additions now penciled in through year-end. Absent a renewed Hormuz disruption, the structural backdrop — rising non-OPEC supply, recovering Middle East flows, and demand growth running well below production capacity — points to further price compression into the second half of 2026. The Strait of Hormuz remains the single variable most capable of invalidating that base case.Geopolitics }}